Source:https://medium.com/

People who don’t practice these basic money habits pay the price.

“Our small, unconscious habits cost us more time and money than we’re aware.”

There is so much content about investing, budgeting, using cash, putting money in envelopes, and other time-intensive or high-level financial techniques. And there are so many people out there reading this content who haven’t even mastered the basics.

People who spend their time thinking about whether they should invest in cryptocurrencies or gold while their credit card companies charge them $200 a month in interest fees. People who try to game stock markets in recession while they continue to defer their mortgage payment.

Look, I get why. Mastering the basics is boring. It’s much more exciting to imagine how much money you could make shorting a stock market crash than it is to imagine how much money you could save in interest by paying off that $6,194 balance on your credit cards. After all, high potential and expediency are the draws of a get rich quick scheme. Because that’s what all this dreaming about high-level financial maneuvers is — fantasies of getting rich quick.

Bad news. There are no get rich quick schemes. Whether you’re an employee with a company-matched 401(k) or an entrepreneur out on their own, the path to wealth is long and slow and full of hard work. And every path to wealth starts with mastering the basics.

So before deciding whether you’re going to invest with a tech-tracked index fund or spring for some Bitcoin, master these fundamentals.

Track Your Expenses

“What’s measured, improves.”

— Peter Drucker

This advice is passed around so frequently that people often feel talked down to, but for all that it’s passed around, it’s rare that anyone actually does it. People think they track their expenses, of course. They pop open their bank app and eye over their last few dozen or so transactions every so often. They keep a close enough eye to figure out when someone’s stolen their credit card. But this casual effort is not enough.

If your expense tracking system can’t…

- Tell you how much you spent per month on food, housing expenses, shopping, gas, and every other major spending category for any given month

- Tell you how much you owe in school loans, mortgages, auto loans, credit card debt, and any other kind of loan in total

- Tell you how much you own in assets, including cars and houses

- Give you an at-a-glance understanding of your financial health for the past six months

…it’s not a good enough financial tracking system.

Your tracking system needs to be able to help you catch the expenses that slip through the at-a-glance, ad-hoc management method.

For example, you might learn from tracking your expenses that you are paying monthly for a service you don’t use (an unused gym membership, for example), in which case you could cancel the service or switch to a cheaper one. Or, you might realize that your habit of dining out or buying clothing from expensive brands is causing you to run out of money by the month’s end.

“Why You Need to Track Expenses to Become Aware of Your Spending” by Miriam Caldwell

What stops many people from graduating from the glance-when-it’s-convenient system is the impression that setting up an expense tracking system is complicated. Articles about personal finance often suggest energy-intensive and sometimes convoluted budgeting systems, like the envelope method or using a kakeibo notebook to record all your transactions by hand.

Those systems may work for dedicated people, but I believe the easiest system is the best system. So if your expense tracking system isn’t cutting it, I recommend Mint.

Mint by Intuit is an expense tracking and financial health platform that 1) is free and 2) takes less than half an hour to set up fully. And after you set it up, it works forever.

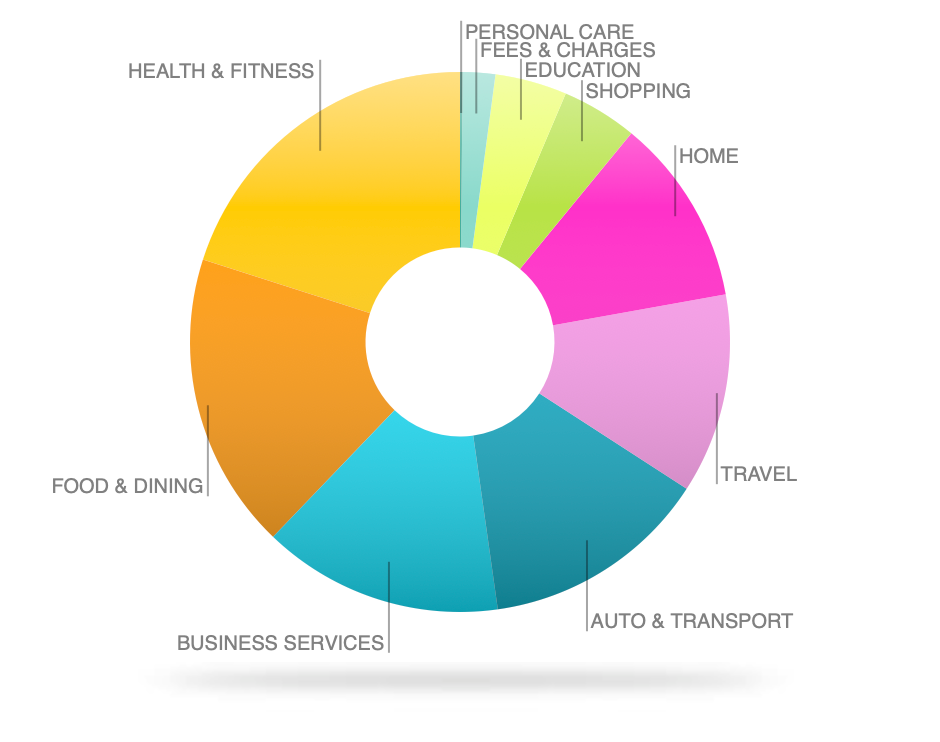

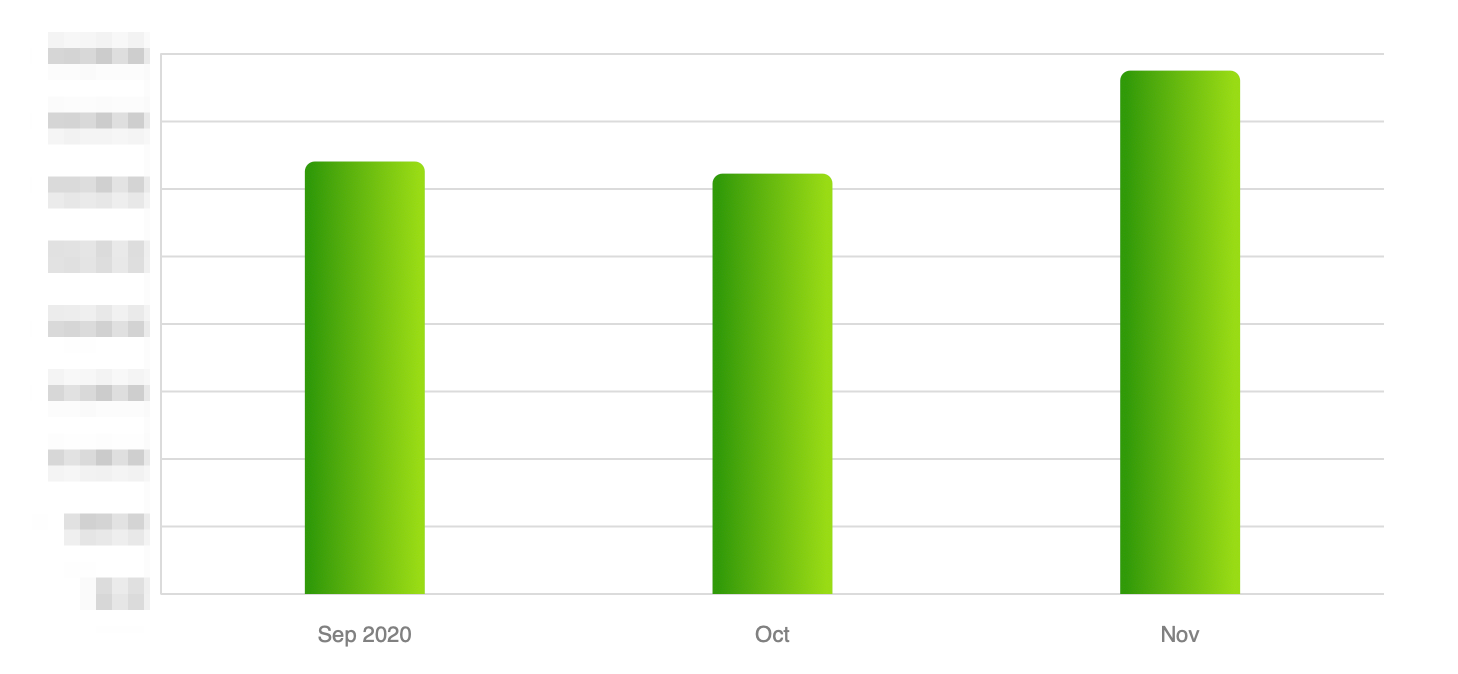

Mint gives you beautiful charts like these:

These beautiful charts can be filtered by expense category, vendor, purchase amount, tags, or any other metric you could humanly want to chart expenses across.

If you want to be more ambitious about your financial health, Mint also does many other cool things like help you keep a budget, track your goals, monitor your credit score, and assess your investment portfolio performance. Mint does so many cool things that I don’t even take advantage of most of them. All for free.

If you don’t have pretty charts like these for your financial health, go sign up for Mint and get some.

Don’t Make Credit Cards Your Default Payment Option

“Beware of little expenses. A small leak will sink a great ship.”

— Benjamin Franklin

One of the most common themes in self-help writing is the scientific finding that humans are terribly irrational. Almost predictably so. That irrationality extends to financial decisions. We rationally know that credit card purchases are not free and that we will have to pay back that balance sooner or later, but we still spend vastly more money when shopping with credit cards versus debit cards or cash.

One of the easiest things you can do to get out in front of your irrational self and save substantial amounts of money is to stop using your credit cards for everything.

Owning credit cards is itself a smart idea. It helps you build credit and gives you a safety net if the world really does fall out from under you. But using your credit cards as your default payment option destroys these benefits. It causes you to run up your balance, trashes your credit, and charges you interest as a reward.

Don’t fall victim to your own irrationality. Take your credit cards out of your wallet. Delete them from your payment options on Amazon, Steam, and any other platform you use. Configure your bills and automatic charges to charge your bank account, not your credit card.

The only time you should be charging something to your credit card is when you mindfully pull your credit card out of your drawer for one and only one purchase.

Change your environment so it supports you and your goals, not the agenda of credit card companies.

Automate Regular Contributions to Your Savings

“A penny saved is a penny earned.”

― Benjamin Franklin

Another area where human irrationality bites us in the ass is contributing to savings accounts. We know we should be saving, we know we should, but saving money provides no instant gratification, so our irrational brains buy things on Amazon instead.

If you don’t have a savings account, you’re not alone. 53% of US households have no emergency savings. Luckily for you, building a savings account is as easy as making a small regular contribution. Pick a small amount, like $50 or $100, and set up a regular bank transfer to withdraw some of your income after every paycheck into a savings account.

Maybe you think you don’t have enough money to deposit even $25 a month. This pandemic has left you too broke to do so. If that’s what you think, go back to that Mint account you just made and look at the lovely chart of your expenses. If you can afford all that pointless bullshit you bought in the last 30 days, you can afford to save a little more.

(If you really can’t afford it, apply for food stamps and Medicaid! Get a representative from your local Medicaid office on the phone, and they can get you approved in no time.)

What you should do with your brand new savings account depends on your financial situation.

- If your credit cards aren’t paid off, use that money to do so.

- If your credit cards are paid off (which I’m guessing they’re not), build an emergency fund.

- If you have an emergency fund (which I’m guessing you don’t), start contributing to your retirement.

Are these habits going to make you a millionaire? No. Are there millionaires who don’t practice these habits? Yes. But the point of practicing these habits isn’t to become a millionaire. The point is to make the most of what you have and to turn it into more.

If you’re not a millionaire, these money habits can keep you fiscally happy and safe. If you are a millionaire, these money habits will only make you even wealthier. From the wealthiest multi-millionaire to the poorest pauper, everyone can improve their life with good money management.

So if you don’t have these money basics mastered, master these before you start trying to read about stock portfolio performance.

You must be logged in to post a comment.